Are you wondering if it's possible to secure a home equity loan with a 500 credit score? Many homeowners find themselves in a financial bind and may need to tap into their home equity for various reasons, such as home improvements, debt consolidation, or unexpected expenses. However, a low credit score can make the process seem daunting. Understanding how home equity loans work and the options available to you can empower you to make informed decisions about your financial future.

In this article, we will explore the intricacies of obtaining a home equity loan with a 500 credit score. We will discuss what factors lenders consider when evaluating your application, alternative options if you're facing challenges, and tips for improving your credit score. Our aim is to provide you with valuable insights and practical advice that can help you navigate this complex landscape.

Whether you're a seasoned homeowner or a first-time borrower, understanding the nuances of home equity loans can make a significant difference in your financial journey. Let's dive into the essential information you need to know to move forward confidently.

What is a Home Equity Loan?

A home equity loan allows homeowners to borrow money against the equity they have built up in their property. Equity is the difference between the current market value of your home and the outstanding mortgage balance. Typically, these loans come with fixed interest rates and predictable monthly payments, making them an attractive option for homeowners looking to access cash for various purposes.

How Does a 500 Credit Score Affect Your Loan Application?

Your credit score is a significant factor that lenders consider when evaluating your application for a home equity loan. A score of 500 is considered poor, which may limit your options and make it more challenging to secure favorable terms. Lenders may view a low credit score as an indication of higher risk, potentially leading to higher interest rates or stricter borrowing conditions.

Are There Lenders That Offer Home Equity Loans with a 500 Credit Score?

While many traditional lenders may shy away from providing home equity loans to individuals with a 500 credit score, some specialized lenders may be willing to work with you. Here are a few options to consider:

- Credit Unions: Local credit unions often have more flexible lending criteria and a better understanding of their members' financial situations.

- Online Lenders: Some online lenders cater to individuals with lower credit scores and may offer competitive rates.

- Private Lenders: Private lenders can be an alternative solution, though they may charge higher fees and interest rates.

What Alternatives Are Available If I Can't Get a Home Equity Loan?

If securing a home equity loan proves difficult due to your credit score, there are alternative options to consider:

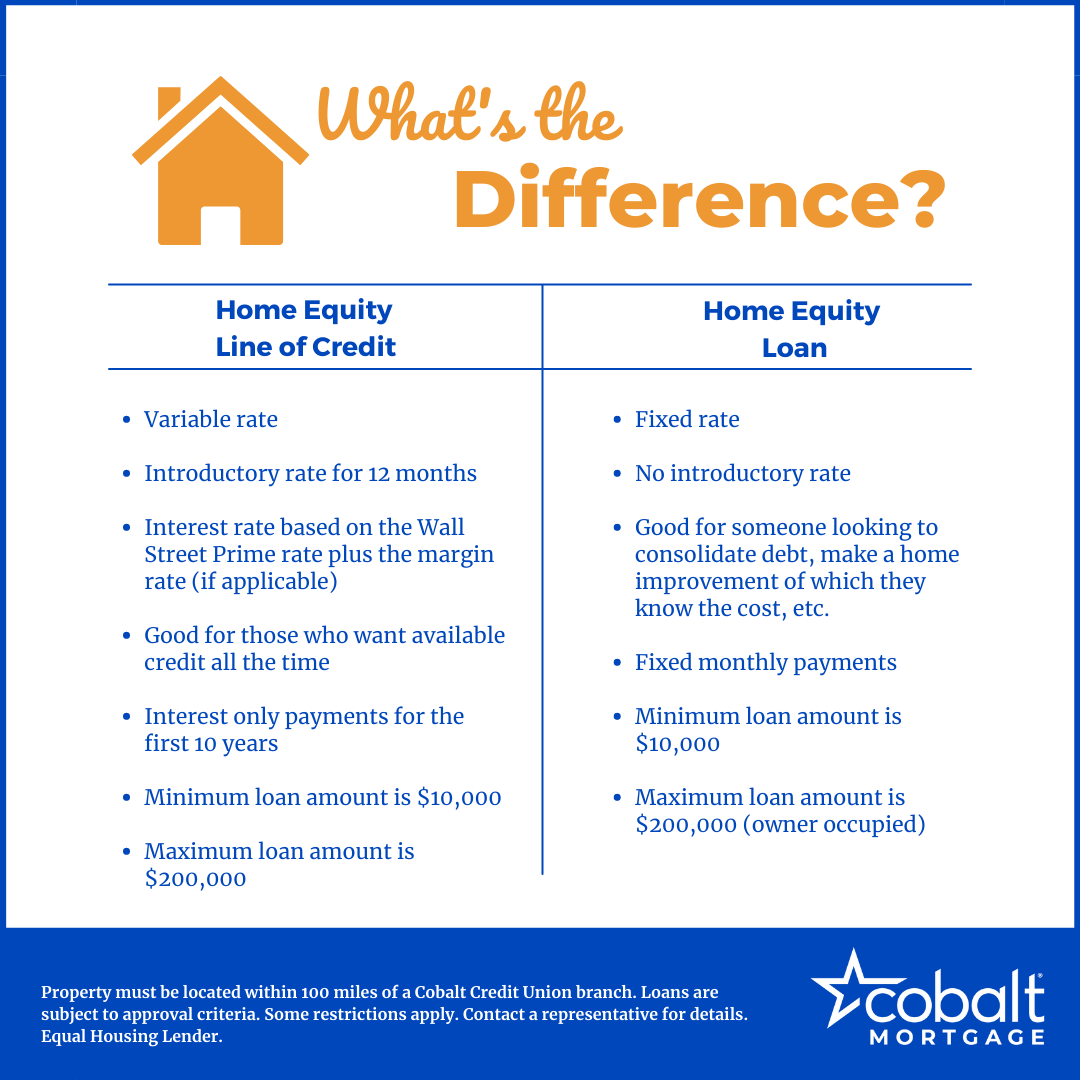

- Home Equity Line of Credit (HELOC): Similar to a home equity loan, a HELOC allows you to borrow against your home’s equity but with more flexibility in borrowing and repayment.

- Personal Loans: Unsecured personal loans may be available, although they often come with higher interest rates.

- Government Assistance Programs: Depending on your situation, you may qualify for government programs designed to help homeowners in need.

How Can I Improve My Credit Score Before Applying?

Improving your credit score can increase your chances of securing a home equity loan with better terms. Here are several strategies to consider:

- Pay Your Bills on Time: Consistently paying bills on time is crucial for improving your credit score.

- Reduce Debt: Aim to lower your overall debt load, especially credit card balances.

- Check Your Credit Report: Regularly review your credit report for errors or inaccuracies that could be negatively impacting your score.

- Limit New Credit Applications: Avoid applying for new credit accounts until your score improves.

What are the Risks of Taking a Home Equity Loan with a Low Credit Score?

While securing a home equity loan with a 500 credit score is possible, it comes with certain risks:

- Higher Interest Rates: You may face significantly higher interest rates, increasing the overall cost of borrowing.

- Potential for Foreclosure: Failing to repay the loan could put your home at risk, as lenders may initiate foreclosure proceedings.

- Limited Loan Amount: Lenders may offer a lower loan amount due to perceived higher risk.

Conclusion: Is a Home Equity Loan with a 500 Credit Score Worth It?

Deciding whether to pursue a home equity loan with a 500 credit score depends on your unique financial situation and goals. While it can provide access to essential funds, it’s crucial to weigh the risks and consider alternative options. By improving your credit score and exploring various lenders, you can enhance your chances of securing the financing you need.

Ultimately, being well-informed and prepared can empower you to make the best decisions for your financial future. If you have further questions or need personalized advice, consider consulting with a financial advisor to explore your options.

:max_bytes(150000):strip_icc()/dotdash-INV-infographic-Home-Equity-Loan-v1-9ae3dc9a5cc141d5a25ed2975c08ea1c.jpg)