When it comes to securing a mortgage, potential homeowners often find themselves at a crossroads: Should they choose a credit union or a traditional bank? This decision is critical, as it can impact not only the terms of the loan but also the overall experience of home buying. Understanding the fundamental differences between credit unions and banks is essential for making an informed choice that fits your financial situation and personal preferences. On one hand, credit unions are member-owned financial cooperatives that often emphasize personalized service and community involvement. On the other, banks are typically larger institutions that may offer a wider array of services but can sometimes lack the personal touch. In this article, we will dive deep into the advantages and disadvantages of obtaining a mortgage from a credit union versus a bank.

As the housing market continues to evolve, so too do the options available for financing a home. With interest rates fluctuating and various lending options available, understanding the nuances of credit union vs bank mortgage becomes increasingly important. Each choice comes with its own set of benefits and limitations that can affect not just your mortgage rate but also your overall financial health. By the end of this article, you will have a comprehensive understanding of which option may be better for you.

Whether you're a first-time homebuyer or looking to refinance an existing mortgage, the decision between a credit union and a bank can be daunting. This article aims to clarify the key differences, helping you to navigate your mortgage options with confidence. Let’s explore the world of credit unions and banks to determine which might be the best fit for your mortgage needs.

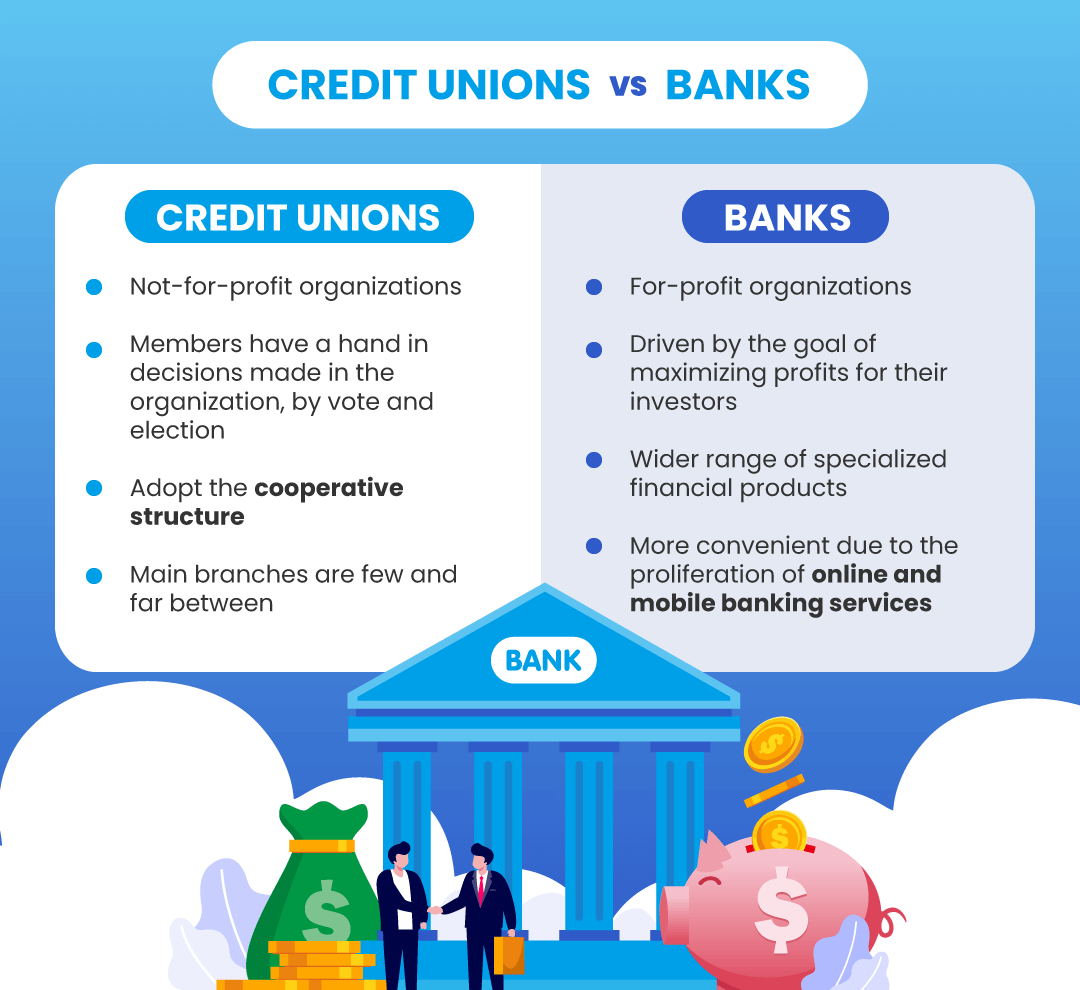

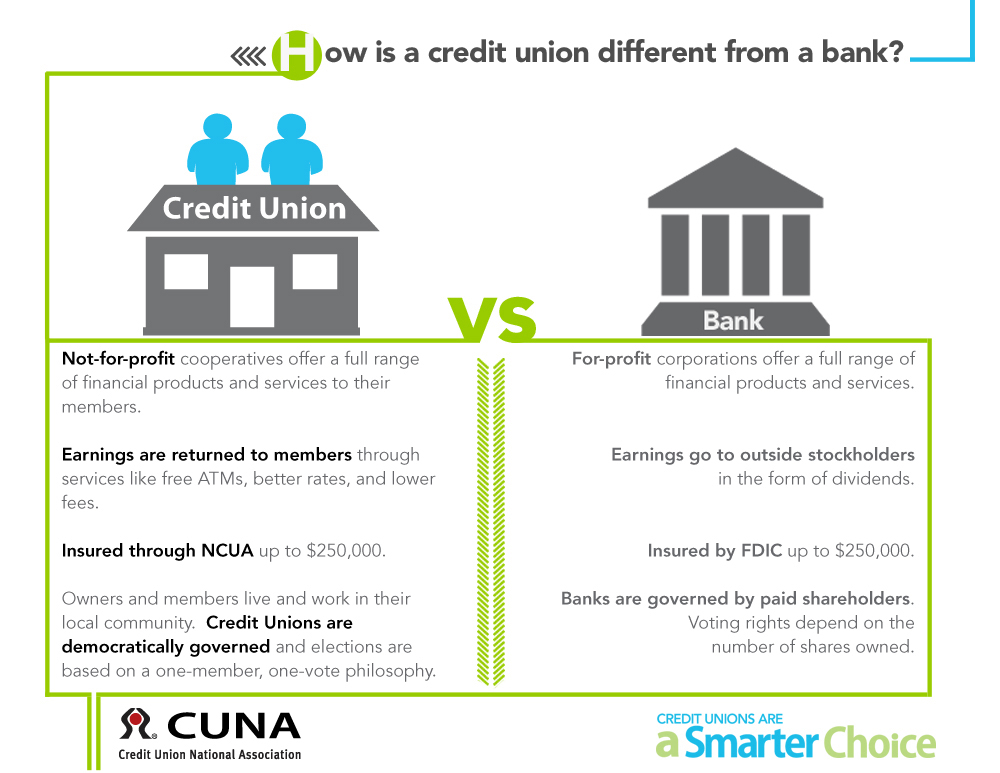

What is a Credit Union?

Credit unions are nonprofit organizations that provide financial services to their members. They are owned and operated by the members themselves, which typically allows them to offer lower interest rates on loans, including mortgages. Since credit unions focus on service rather than profit, they often prioritize member satisfaction and community engagement.

What is a Bank?

Banks, on the other hand, are for-profit institutions that offer a variety of financial services, including savings and checking accounts, personal loans, and mortgages. They tend to have more branches and ATMs compared to credit unions, which may make them more accessible for some customers. However, their focus on profit can sometimes lead to higher fees and less favorable loan terms.

How Do Mortgage Rates Compare Between Credit Unions and Banks?

One of the most critical factors when choosing between credit union vs bank mortgage is the interest rate. Generally, credit unions can offer lower mortgage rates compared to traditional banks. This is largely due to their nonprofit status and member-focused business model. Here are some comparisons:

- Credit unions typically have lower average mortgage rates.

- Banks may offer promotional rates, but they often come with additional fees.

- Both credit unions and banks may vary their rates based on your credit score and financial history.

What Are the Fees Associated with Mortgages?

Fees can significantly impact the total cost of a mortgage. Credit unions often have lower fees for mortgage origination and closing costs compared to banks. Understanding these fees can help you make an informed decision.

What Fees Should You Expect?

- Application fees

- Origination fees

- Closing costs

- Prepayment penalties

Before deciding on a lender, it's wise to ask about all associated fees to avoid surprises down the line.

How Does Customer Service Differ in Credit Union vs Bank Mortgage?

Customer service is another area where credit unions often excel. Being member-centric, credit unions usually offer personalized service, whereas banks may adopt a more standardized approach. You are likely to experience shorter wait times and more individualized attention at a credit union.

What Should You Expect in Terms of Service?

- Friendly, personalized service at credit unions.

- More bureaucratic processes at banks.

- Longer response times from larger banking institutions.

Are There Membership Requirements for Credit Unions?

Unlike banks, credit unions often have membership requirements, which can vary widely. Some may require you to live in a certain area, work for a specific employer, or belong to a particular organization. Understanding these requirements is crucial if you are considering a credit union for your mortgage.

What are Common Membership Criteria?

- Geographic location

- Employment within a specific industry

- Membership in an affiliated organization

Which is Right for You: Credit Union vs Bank Mortgage?

The choice between a credit union and a bank for your mortgage ultimately depends on your financial situation, preferences, and needs. If you prioritize lower rates, fewer fees, and personalized service, a credit union may be the better option. Conversely, if you prefer a broader range of services and more extensive branch access, a bank might suit you better.

Conclusion: Making the Right Choice

In the battle of credit union vs bank mortgage, both options have their merits and drawbacks. By understanding the key differences, you can make a more informed decision on which lender will best meet your mortgage needs. Remember to consider factors like interest rates, fees, customer service, and eligibility requirements before making your choice. Ultimately, your goal should be to find a mortgage that aligns with your financial goals, ensuring a smoother path to homeownership.

:max_bytes(150000):strip_icc()/dotdash-credit-unions-vs-banks-4590218-v2-70e5fa7049df4b8992ea4e0513e671ff.jpg)